Fed Rate Cut 2025: What It Means for Florida Homebuyers & Sellers

Fed Rate Cut: How It May—or May Not—Benefit Florida Real Estate

The Federal Reserve cut its benchmark rate by 0.25% on September 17, 2025. Here’s what that could mean for mortgage pricing, inventory, and your timing in Central Florida—backed by verifiable sources and local strategy.

What Actually Changed on Sept 17, 2025

Source: Federal Reserve FOMC statement (verify on federalreserve.gov).

Mortgage Rates Now vs. the “Fed Rate” (Know the Difference)

Mortgage pricing tracks longer-term bond yields and market expectations. Weekly surveys showed 30-year averages easing into and after the meeting. Day-to-day changes are normal; the trend matters more than a single print. (See Freddie Mac PMMS; MBA Weekly Apps.)

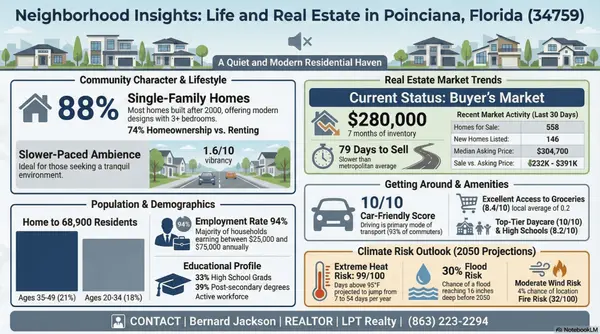

Florida-Specific Impact: Affordability, New-Build Incentives, Inventory

Affordability snapshot (illustrative)

- Lower rates can expand qualifying power

- Pair with seller credits and DPA where eligible

- Micro-market comps ≫ state averages

We’ll run real numbers for your credit, DTI, and product.

Builders & incentives

- Widespread buydowns and concessions

- Selective price reductions where needed

- Timing leverage for ready buyers

Cross-check NAHB and reputable trade publications.

If You’re Buying (Poinciana • Kissimmee • Davenport)

- Lock a rate window while you shop. Pre-approval makes dips actionable.

- Stack incentives: builder buydowns + seller credits + lender credits (e.g., RP Funding-style closing-cost strategies where suitable).

- Target micro-markets (school zones, HOA/no-HOA, commute corridors) instead of averages.

- Refi plan: If rates drift lower later, consider refinancing when the math pencils out.

Florida lenders frequently structure closing-cost credits to reduce cash-to-close—useful for renters transitioning to owners. (Example positioning: Robert Palmer / RP Funding.)

If You’re Selling

| Move | Why It Works Now |

|---|---|

| Price to today’s comps | Values moderated from peak; comp-anchored listings win showings. |

| Offer credits/buydowns | Expand buyer pool without repeated price cuts; match new-build playbook. |

| Leverage momentum | Application spikes often coincide with lower-rate weeks—maximize exposure. |

Risks & Realities (No Magic Wand)

- Inflation/yield risk: If markets fear re-acceleration, mortgage rates can bounce even during a Fed cutting cycle.

- Labor softening: Confidence can wobble if job data weakens further.

- Inventory lock-in: Many owners hold sub-6% loans; supply improves gradually, not overnight.

FAQs

Did the Fed cut rates this week?

Yes—by 0.25% on Sept 17, 2025 (see Federal Reserve statement).

Will Florida mortgage rates drop right away?

They’ve eased recently, but mortgage pricing follows longer-term yields and expectations. Daily moves vary.

Is now a better time to buy?

Lower rates plus incentives improve affordability for prepared buyers. Let’s get you pre-approved and compare scenarios.

What if rates fall later?

We’ll map a refinance decision tree—if the savings net-net beats costs, you capture the improvement.

Book Your Plan

About Bernard Jackson Jr. — Bilingual REALTOR® with LPT Realty serving Poinciana (34758–34759), Kissimmee, Davenport, Winter Haven, and Lake Wales. I specialize in helping renters become homeowners with strategic financing, builder incentives, and data-driven negotiation. Call/text (321) 443-5582 • bernardjacksonrealtor@gmail.com • Read reviews.

¿Listo para pasar de inquilino a propietario en Florida Central? Poinciana (34758–34759), Kissimmee y Davenport: te ayudo con precalificación, incentivos de constructor y créditos para costos de cierre. Agenda tu consulta.

Categories

- All Blogs (210)

- #FearlessFriday (10)

- #MotivationalMonday (14)

- #solutionsaturday (6)

- #SoulfulSunday (7)

- #TechnologyThursday (10)

- #WellnessWednesday (14)

- 10 Steps To Know About Buying A Home In Poinciana (1)

- 10 Things To Know About Davenport (1)

- 10 Things To Know About Poinciana (2)

- 5 New Things For Poinciana For 2025 (1)

- Annual Events and Festivals in Kissimmee, Fl (2)

- Benefits of Living in Poinciana (2)

- Benefits of Selling to a Cash Buyer (1)

- Buyers (79)

- City Guides Kissimmee (16)

- CITY GUIDES: Poinciana Real Estate News & Resources (6)

- CITY STATISTICS: Davenport Real Estate News & Resources (1)

- City Statistics: Kissimmee (2)

- CITY STATISTICS: Lake Wales Real Estate News & Resources (1)

- Kissimmee Homes For Rent (5)

- Kissimmee Homes For Sale (9)

- Pros and Cons of Living in Kissimmee, FL (1)

- Renters (37)

- Retirement In Poinciana, FL (1)

- Sellers (17)

- Things To Do In Poinciana (2)

- Things To Do Near Kissimmee, FL (2)

- Things To Do NYE 2025 In Orlando and Kissimmee, FL (1)

- Truth About 20 Percent Down (1)

- What Are The Benefits of Living In Kissimmee (1)

- Your Dream House (2)

Recent Posts

GET MORE INFORMATION